Homebuyers have had it tough lately, suddenly finding themselves in a sellers market as summer came along. And mortgages suddenly cost more too -- when you could even get one. But of course Thanksgiving isn't about looking at negatives. So, if you can, look past that elephant-in-the-room that is the credit crunch and take stock of what's now on the table for those homebuyers with the capital.

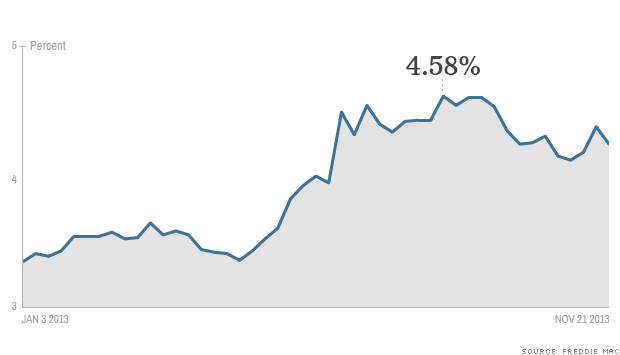

Low Mortgage Rates: Yes, mortgage rates rose year, along with home prices, but rates are still at historic lows (we are constantly assured) and have been sinking in recent weeks. Can housing prices be far behind? If you are really ready to buy, those Black Friday bargains are small potatoes compared to what you might save by shopping right now in real estate's historically slow season[2] -- especially from sellers who saw summer's homebuying frenzy pass them by.

A Bidding-War Cease-Fire: The heated bidding wars that have been witnessed in some real estate markets -- especially in California -- reportedly have cooled with weather and amid rumors that sellers were deliberately underpricing their homes[4] to encourage competing bids. And although home prices continued to climb[5] as summer drew to a close, it was at a slower pace. Meanwhile, the number of Americans applying for home loans[6] has plunged.

Weary and Wary Investors: Speaking of the competition, the real estate speculators appear headed for the sidelines after years of swooping in to snatch up bargain properties with ready cash. A recent poll of investors[7] found that only around 1 in 5 are still interested in buying more homes -- about half the number from a year ago. For average home-shoppers that means less competition from a preferred class of homebuyers. Meanwhile, those foreign investors who were reportedly buying Florida property sight-unseen[8] at the beginning of 2013 (and even giving Detroit a nibble) might have moved on to Portugal and Spain[9], where 3 million homes lie vacant and the governments are ready to barter with tax incentives and visas.

The 'Nuclear Option': What does the real estate market have to do with the recent change in the U.S. Senate's filibuster rules[10]? It means that Rep. Mel Watt (D-N.C.), the Obama administration's nominee to head the Federal Housing Finance Agency[11] might finally be confirmed. And if that happens -- and it's only a glimmer of a possibility at this point -- Watt might drop plans to lower the ceiling on the amount of money[12] available for government-backed mortgages. Ideological and political conflicts aside, that would be good news right now for homebuyers who might otherwise not be able to afford their dream homes.

The Latest Technology: In many ways technology has made home shopping easier than ever -- much less dependent on guesswork and reliance on third parties -- and it only seems to be getting more convenient. Along with smartphone apps for homebuyers[13] (many of them free) that calculate mortgage payments and estimate home values, there's at least one that instantly accesses information about a home just by taking a snapshot of it with a smartphone camera. Others detect homes with recent price reductions; screen for upcoming open houses; rate neighborhoods on the basis of crime rates[14]; and do the numbers based on "lifestyle"[15] -- such as how much it might cost to commute to work from a new location. So even if you aren't ready or able to buy, some of these apps can aid in a search for a rental.

Source : http://realestate.aol.com/blog/on/reasons-home-buyers-thankful-2013/